Service Demand in Local Trades

- James Isaacs

- Mar 22

- 8 min read

The question behind Ostix

The idea behind Ostix did not begin with marketing. It began with a simpler question: Why do so many service industries remain unstable even when the underlying need is obvious?

Firms work hard, the need is real enough, yet margins stay thin, teams are hard to hold together, and competition repeatedly collapses back toward price. Arboriculture was one starting point, but the same pattern appears in landscaping, building maintenance, exterior cleaning, and many other local service trades.

These problems are usually discussed as though they are separate. Marketing is treated as one issue, labour as another, pricing as another, and competition as something sitting off in the background. Over time, it has become harder to see them that way. In many cases, they are not separate problems at all. They are different expressions of the same underlying structure.

This article sets out that structure in simple terms.

Demand often exists before marketing begins

In many local service markets, the need appears before any promotion does.

A hedge has become unmanageable. A retaining wall is failing. A roof leak has to be dealt with. A tree is threatening a house or needs professional assessment before further work is done. A property has to be brought under control before sale.

In cases like these, the problem comes first. The search for a provider follows.

That changes the role of marketing. The job is not usually to create desire from nothing. It is to influence how a business is interpreted when existing need enters the market.

That may sound like a small distinction, but it changes almost everything. If demand is already forming, then the real issue is not simply how much attention a business can generate. It is how that business is read when the customer begins comparing options.

Local service demand is not one thing

Many service businesses speak about “the market” as though it is a single pool of buyers. It rarely is.

Within the same broad service category, different forms of demand are often present at the same time. Some buyers are heavily price-driven. Others are trying to reduce uncertainty and want somebody reliable, professional, and easy to deal with. Others are dealing with larger, riskier, more technical, or more visible jobs and are looking for a higher level of capability.

These are not just different personalities, they are different demand conditions.

A homeowner looking for the cheapest hedge trim is not evaluating providers in the same way as a property owner dealing with a dangerous tree near a house, or a commercial client trying to avoid disruption and reputational risk. The work may sit under the same service category, but the basis of choice is not the same.

This matters because businesses are not simply competing for more demand. They are being sorted into different parts of the market depending on how they appear at the point of evaluation.

Why good firms still get treated like general providers

A persistent problem in fragmented service industries is that capable firms often present themselves too broadly.

Their services are described in general language. Their websites look interchangeable with other firms in the area. Their proof is weak, generic, or inconsistent. Their differences may exist in reality, but they are not visible enough when the customer is comparing options.

Once that happens, the market has little choice but to read them as general providers.

That is where price competition becomes most intense. A business may genuinely be more organised, more experienced, or more capable than much of the field, but if those distinctions are not visible at the point of selection, they do not materially change how the market sorts it. The firm gets dragged into comparison with everyone else who looks broadly similar.

This is one reason strong operators can still feel trapped in mediocre economics. The capability may be real, but the market does not always recognise it in time.

Fragmented markets push firms towards interchangeability

This becomes even more important in local service industries with relatively low barriers to entry.

Experienced workers can often leave employment and start operating with modest capital. That creates a large number of small firms competing in the same geography. From a distance, that can look like healthy competition. In practice, it often produces a crowded market full of businesses that are only weakly differentiated from one another.

The more interchangeable those businesses appear, the more selection falls back on the easiest visible criteria:

Price

Speed

Availability

Superficial reassurance

That is not because customers are irrational. It is because the market is forcing them to compare on what is easiest to see.

This is where marketing, positioning, proof, and service framing become economically meaningful. They are not cosmetic extras. They help determine whether the business is interpreted as a generic provider or as something narrower and more defensible.

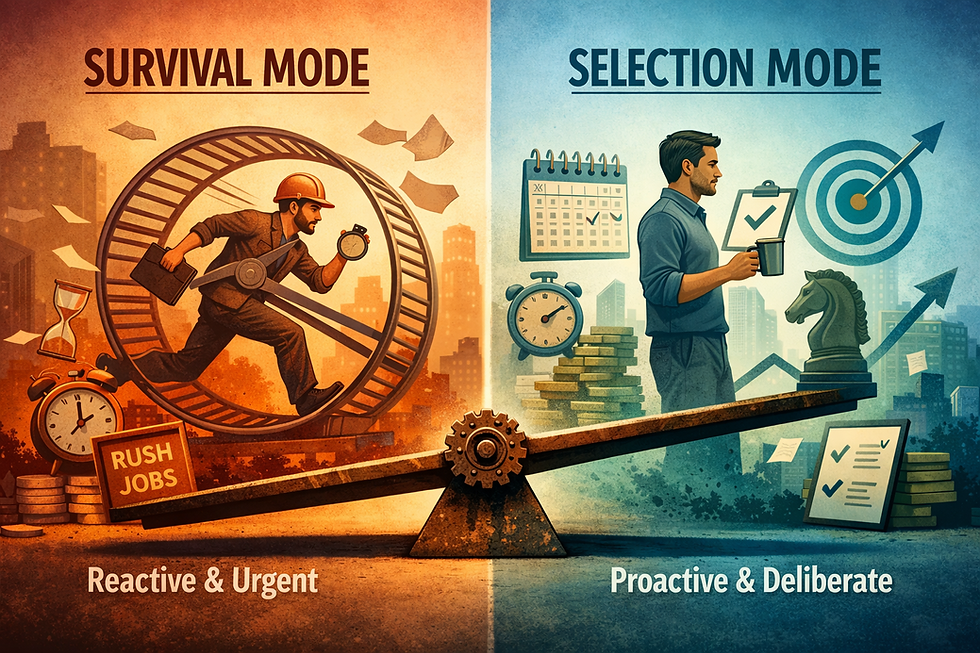

Selection mode and survival mode

A useful way to think about this is the distinction between selection mode and survival mode.

Survival mode

A firm operating in survival mode is not really selecting. It is absorbing whatever work it can get.

This often follows pressure of some kind: a downturn, staff loss, debt, failed expansion, weak margins, or a decline in enquiry quality. Under those conditions, the business broadens rather than sharpens. It says yes too often. It accepts weaker-fit clients, more price-sensitive work, and jobs that do not align well with its strengths.

The website becomes broader, not tighter. The offer becomes more general, not more distinct. The language becomes more accommodating, not more selective.

In effect, the business moves closer to the most interchangeable part of the market at exactly the moment it most needs to escape it.

Selection mode

A firm in selection mode behaves differently.

It has enough stability to refuse misaligned work, enough margin to reinforce the capabilities it actually wants to be known for, and enough internal confidence to signal itself more narrowly. It is not merely trying to increase demand. It is trying to influence the type of demand most likely to reach it and convert.

This is where positioning starts to matter in a practical sense. A business that can select is better able to preserve coherence between what it does well, what it signals to the market, and the kind of work it attracts.

That coherence is often what separates a firm with direction from a firm that is merely busy.

A concrete example from the trades

Take a local arborist business.

On paper, it may offer tree removal, pruning, hedge work, stump grinding, and general maintenance. If all of that is presented in flat, generic language, the business risks being interpreted as just another tree company. At that point, it will tend to be compared on price, responsiveness, and availability.

But not all tree work is the same.

Some customers want the cheapest possible job. Some want a careful operator who will protect structures, communicate well, and leave the site tidy. Others want an experienced crew capable of handling large or technically difficult work without unnecessary risk. Those are different demand conditions, and they do not all reward the same provider.

If the business is genuinely stronger in higher-trust, higher-judgement work, then broad generic signalling can become a trap. It attracts too much of the wrong demand and not enough of the right kind.

The same logic applies beyond arboriculture. A landscaping firm, builder, maintenance contractor, or exterior cleaning business may all experience the same structural issue. The problem is not always a lack of demand. It is often that the business is being sorted into the wrong part of the market.

Marketing is part of the market’s sorting process

Seen this way, marketing is not primarily a volume mechanism.

It is part of the market’s sorting process.

Reviews, service-page structure, language, imagery, proof, visible standards, and the way work is framed all help determine how a business is classified when a customer starts comparing options. Weak or generic signals push the firm towards the broad pool of comparable providers. Stronger and more coherent signals make it easier for the market to place that business in a narrower segment where the basis of competition is different.

That does not mean every firm should become more niche in a simplistic sense. It means the business needs to be more legible to the kind of demand it is actually best suited to serve.

This is also why doing more marketing often disappoints. More activity does not automatically improve market position. If the signals being amplified are still broad, weak, or confused, then more activity may simply spread the problem further.

Why labour, pricing, and marketing problems often cluster together

Once the sorting logic is visible, a number of common business problems start to look less separate.

Price pressure is not just a pricing problem. It is often the result of weak differentiation inside a fragmented market.

Staffing problems are not just labour problems. They are often tied to margin compression, unstable work mix, and the inability to sustain a stronger operating model.

Poor marketing results are not always caused by low activity. In many cases, the business is simply competing in the wrong part of the market, with signals too weak to support anything better.

This is why local service businesses can feel stuck. They are often trying to solve downstream symptoms one by one, while the upstream sorting problem remains untouched.

What local service businesses can actually do

A single firm cannot redesign the entire market. Fragmentation, entry pressure, and wider economic conditions will remain features of many service industries.

But that does not make the business powerless.

One of the few practical levers still available is the ability to influence how the market reads the firm. That means being more precise about what the business is actually well suited to do, strengthening the visible signals around that capability, and becoming more deliberate about the kind of demand it is willing to serve.

In practical terms, that may involve:

Tightening service-page language

Showing stronger proof of the kind of work the business wants more of

Reducing broad, generic claims

Presenting the business in a way that matches its real strengths

Making it easier for better-fit customers to recognise the difference

None of that guarantees immediate transformation. But it does improve the odds that the business is evaluated on more useful terms.

Why this matters

This is why marketing matters here, but not in the inflated way it is often discussed.

In fragmented local service markets, marketing is one of the few practical levers available to help move a firm out of survival mode and towards selection mode. It cannot repeal the structure of the market, but it can change where the business sits within it.

Once that shift begins, other things often start to move with it:

Pricing tolerance

Work quality

Staff stability

Client fit

Long-term direction

That is the real interest in service demand. Not simply how to generate more of it, but how to be sorted more advantageously when it appears.

Get in Touch

If this feels familiar, the issue may not be a lack of marketing activity. It may be a deeper question about how your business is being interpreted in the market, what kind of demand it is attracting, and where it is being pulled into the wrong kind of competition.

That is usually an Ostix Engagement problem before it is a channel problem.

In some cases, this is less about a major repositioning exercise and more about steady monthly improvement to the signals customers already use.

Comments